Fixed assets. So simple, but always the problem child.

There are two main problems you will face with fixed assets. One is that it is one of the rare DTA/DTL with two dueling side by side reconciliations. Most other DTA/DTLs are either one basis only (like stock based comp or Right of Use assets), or one where you can start with GAAP and make adjustments to get to Tax basis (like prepaids, deferred rev, etc). And the rollforward supporting schedules most likely contain MORE than just fixed assets for GAAP, muddying up what you are analyzing.

The second problem is that fixed assets is so easy to shortcut the full balance sheet reconciliations and do via income statement method (gains and loss, and depreciation expense differences).

Why would these be problems? Because we like to book random stuff to fixed asset GAAP income/expense accounts that don’t belong and causes variances in our DTA/DTL.

The easy fix? Make sure you are cleaning up DTA/DTL balances on a routine basis using the RTP. And don’t use income statement method blindly.

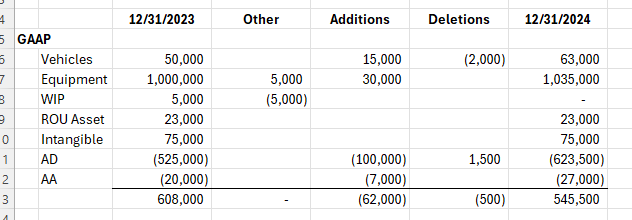

Before you start creating your GAAP vs Tax reconciliation, think about what you have. Here above is a screen shot of what might be a high level support for GAAP. Note that there is Work in Process (WIP). While the tax and GAAP basis for this item may be the same, you are likely to be pulling the tax depreciation from system files for which WIP has not been added because it is not yet depreciable.

Note also the inclusion of intangible assets and ROU Asset. Maybe you decide you will make this a fixed asset/intangible support reconciliation. But looking closer you can see one accumulated amortization account, meaning you are going to have to dig deeper to split out ROU amortization from regular old intangible.

At this point, I make a plan and WRITE IT DOWN in little notes to the side of the reconciliation. Here, I would remove intangibles and just do its own reconciliation separately, and I would make a plan on how I will include WIP on tax recon, but show how we adjust out to get back to tax schedules not yet adding WIP to the depreciation system, because reviewers like things to tie out to supporting schedules.

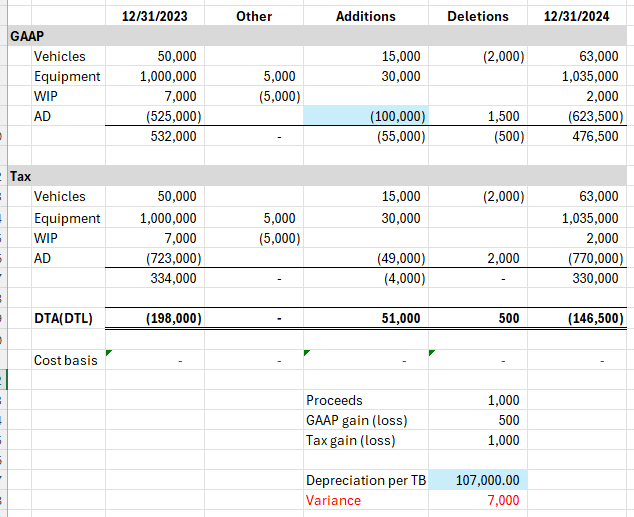

After cleaning up the GAAP schedule to show just fixed assets and updating tax return software for current year additions and deletions and obtaining the tax book values for the year, I have the above comparison. Note I have a check figure for cost basis between the two basis. If there is a legit difference, you will want to track and explain why.

I like to source any proceeds received on disposals and do a quick calc of the two basis gain/loss. A lot of time, GAAP doesn’t match expectation to what is in the TB.

Note that what is in the TB for depreciation is not what is shown in the actual rollforward. So I go back to my audit group and ask them why, to which the respond “immaterial, pass.” I know that my reviewer likes to look at fixed asset from the income statement approach using the TB, rather than the rollforward of the balance sheet accounts. Let’s see how this plays out.

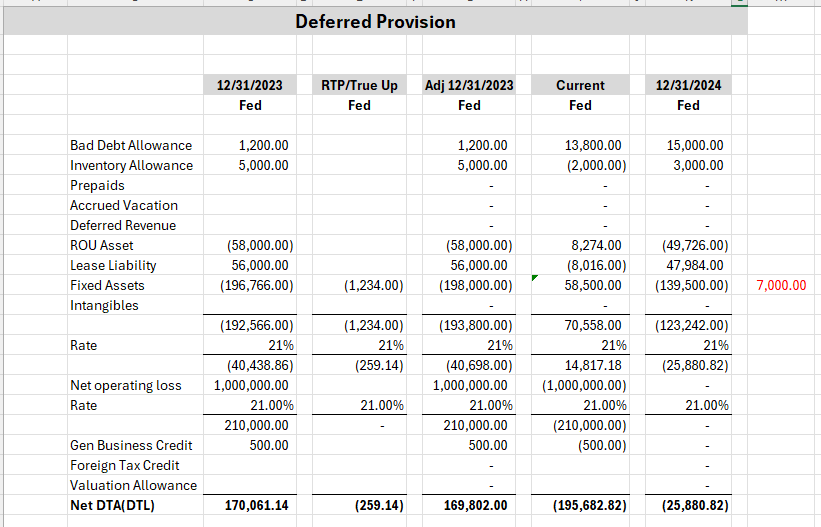

First, notice that my beginning DTL on the deferred provision doesn’t match detailed tie out. So the first thing I do is fix this (credit DTA account, debit deferred tax expense and make sure on my TARF this lands on the RTP line item). I now tie to the 12/31/2023 balance of 198,000.

Note that the total change in the DTL for the year is 51,500 on the detailed reconciliation (using balance sheet approach). Using the income statement approach, it looks something like this:

The difference? The $7,000. And since we have used the income statement approach in the deferred provision (58,500), our ending DTL reflects 139,500 when in actuality it is 146,500.

In fact, this $7,000 will create a minor adjustment next year, just like the 1,234 did for this year.

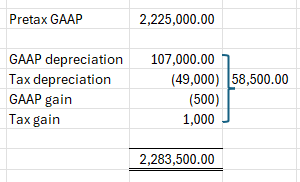

What’s the fix? Very clearly document to your reviewer why you are using the GAAP depreciation amount of 100,000 instead of the TB amount of 107,000. Spoke to auditor, amount immaterial so passed on investigation. As amount is different than depreciation expense needed to roll forward fixed asset net book value, difference is likely a fixed asset ancillary expense (example could be sales tax booked erroneously to depreciation expense).

This variance may also be occurring in the GAAP gain/loss on fixed asset disposal account.

Dealing with these rollforward vs what in TB account issues on the GAAP side will go a long way toward making fixed asset DTA/DTL straight forward.