Return to provision – an adjustment between the tax provision as recorded in the issued financial statements and the results taken on the filed tax return due to best estimate rather than actual used at provision time.

An example of a true RTP is the difference between vacation estimated to be taken by 3/15 when the financial statement was issued in early February. By the time to return is filed, we know exactly what the deduction will be.

An example of what a true RTP is not is the mistake you made in failing to correctly calculate deferred revenue adjustment at the provision, which was caught at tax return time.

Mostly we use the term RTP losely to denote:

- True RTP caused by legitimate estimates, material or immaterial

- immaterial booboos or immaterial things we estimated because we had information but were lazy or rushed.

So, obviously not the true definition of an RTP. This is why I like to refer to this group as “RTP/PY Cleanup”, and lets be honest, its 95% immaterial adjustments for PY booboos. Because “immaterial, pass” is your friend when time is short.

How does one calculate the RTP?

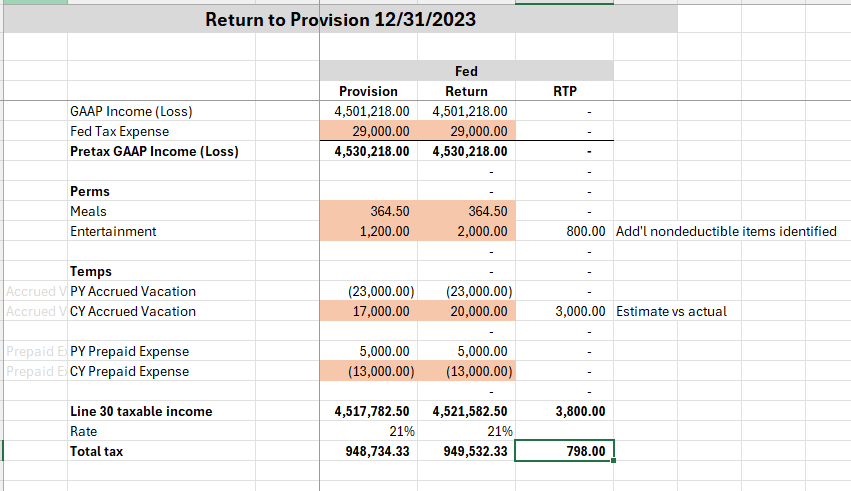

1. Figure out total adjustments. Take the prior year current provision in its entirety and compare to the filed tax return. Here’s a nice short example of what that would look like. I generally do this when I prepare the tax return (so RTP is being knocked out at the same time as tax return prep). Do reviewer a favor, add comments on what created the difference.

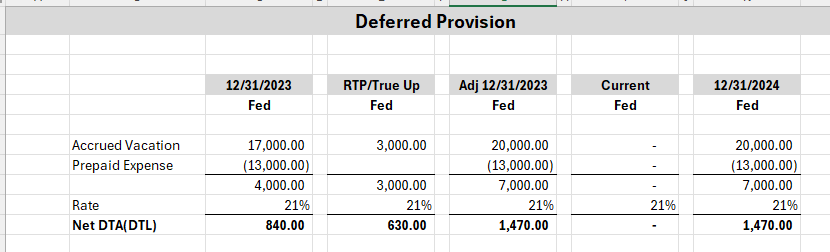

2. Update any temporary items to your Deferred Provision. For our accrued vacation, we want to adjust that 2023 ending balance from 17,000 to 20,000. Note this gives us a deferred tax expense effect of $630 (debit DTA, credit deferred tax expense). Do this same adjustment for all temporary items. Place total on the TARF, RTP Deferred Provision line (see below).

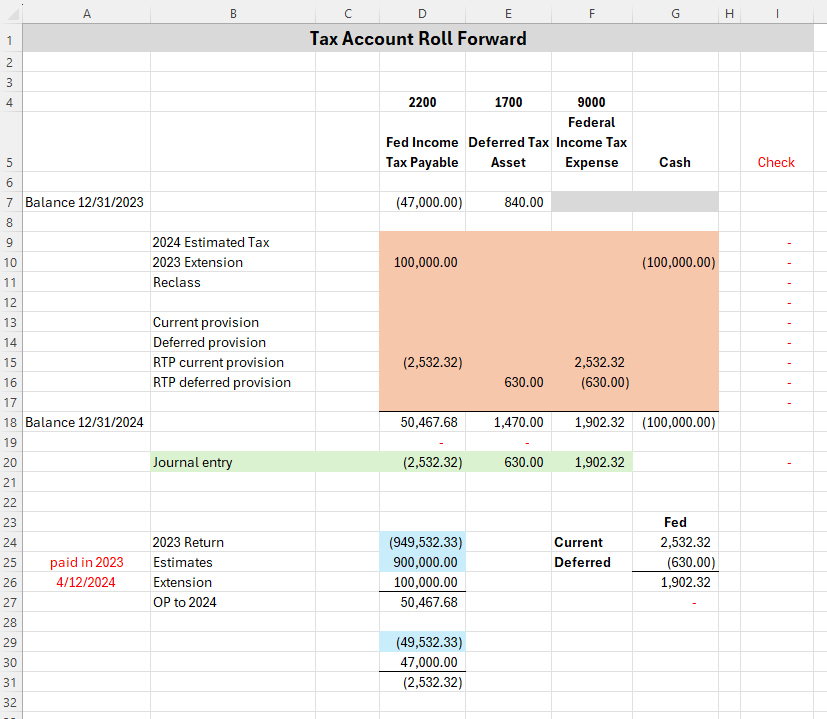

3. Reconcile taxes payable/receivable account to PY tax return.

I know this seems confusing. We just did work on adjusting all the temporary items, shouldn’t we be adjusting all the permanent items now? Unlike the Deferred Provision, there is no rolling schedule of permanent items.

Think big picture here, and go back to the lesson on how tax provisions work from a closed system. We just trued up DTA account which necessitated an item by item approach. We are now cleaning up Taxes Payable/Receivable which only needs to agree back to the tax return (and any subsequent estimate tax payments or refunds).

Throw down a reconciliation (I like to do this on TARF) of what the overpayment to the 2024 tax return should be. From this amount, figure out what should have been booked as the tax payable/receivable at 12/31/2023, which is the blue amount of 49,532, and 2,532 difference from the 47,000 actually recorded. (The 100k of extension payment wasn’t paid until 2024, see where we include on row 10).

Why does this not match the $798 from our RTP in step #1? Because someone last year forgot reconcile the ending. I see this almost every time I do a new-to-me provision. I find it easier to prove out what I’m doing in one clean figure that ties back to expectation per return.

4. Adjust Deferred Provision RTP/Clean up as needed. As you complete the present provision process, you will of course tie out each ending DTA/DTL back to an ending check figure. And as you do so, you will find some items that are slightly out of balance, due to the prior year person skipping this critical tie out step. As you find items, pop them into the Deferred Provision RTP columns (remember to reference/comment these figures).