These two items are the #1 driver of immaterial reasons your rate rec and expense proofs won’t tie to actual expense and they will make you want to pull your hair out.

Why?

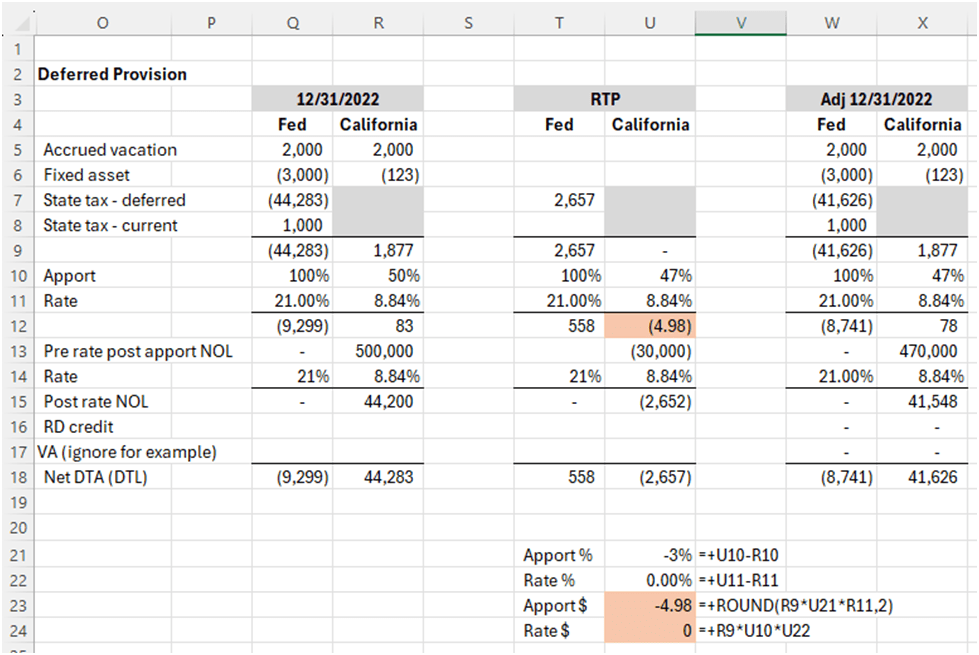

ASC 740 says we must value the DTAs/DTLs at the enacted amounts that will unwind in the future. So if in 2022 my California apportionment rate was 50% and all I had was a DTA for vacation accrual, in 2023 when my activity in California has pushed my apportionment rate down to 40% and I unwind (use) the vacation DTA as a deduction, it HAS to come off at 40% because that is my apportionment rate from the year. Which means I HAVE to somehow account for this step down from 50% to 40% in my deferred schedule, and then unwind it.

Want to make it more confusing? Say 2022 provision we estimated apportionment to be 50%, but it was actually 47% per the 2022 tax return, but for 2023 provision we are estimating the apportionment to be 40%. That’s two different adjustments that you need to make in the present provision. I do this below in orange, and then just tack a +U23+U24 to the end of the formula in cell U12.

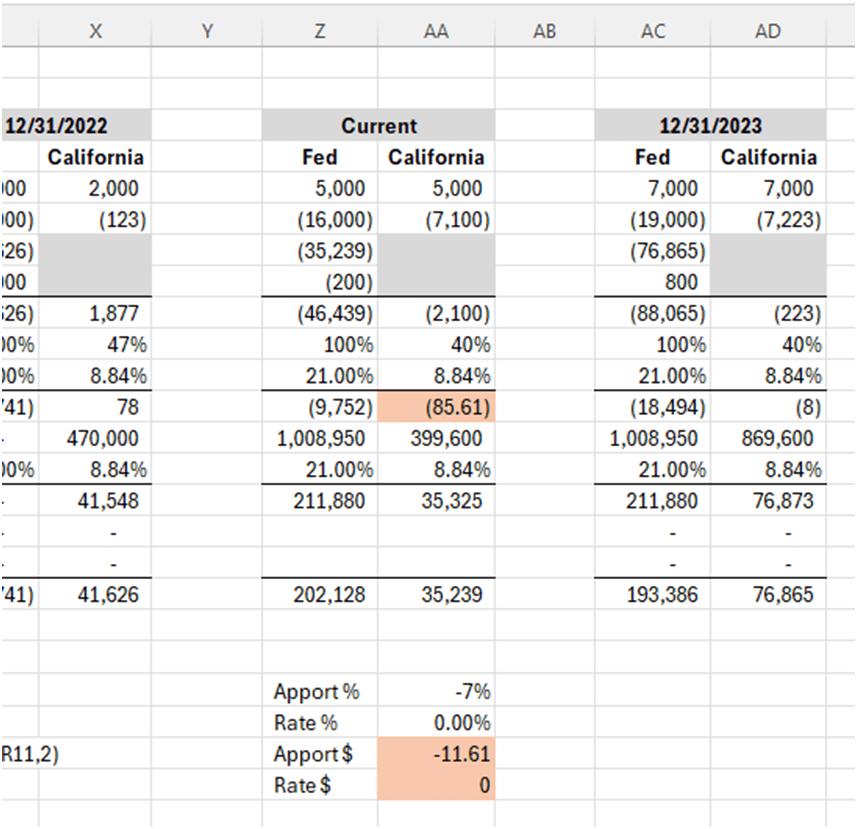

And then literally the same thing to step down again to the 40% apportionment:

Let’s say you have multiple states and use a blended rate. Process is still fundamentally the same. You have estimated apportionment & rates used in previous provision, the actual per the tax return, and what you estimate the present provision apportionment and rates to be. You can math it out, and figure out the actual adjustments, but wrap it all up into a blended rate which is on a separate support tab and the final blend % pulls into the Deferred Provision.

But did you apply this blended rate step up/step down to any NOL DTAs? If yes, let me explain your next headache.

NOLs and Blended Rates

For MOST states, net operating losses are PRE tax, but POST apportionment. There are a few anomalies out there, but for the most part this holds true. See CA Form 100 below, note line 18 is post apportionment. Note line 19 is the use of prior year NOLs, and that it, too, is post apportionment, pre tax.

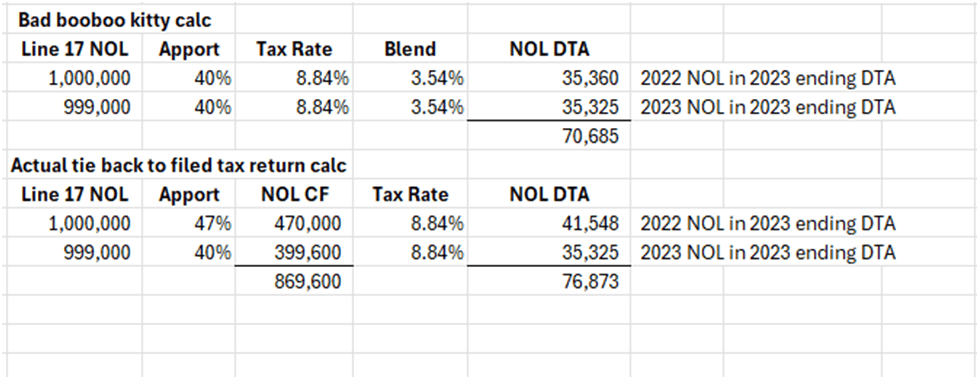

Let’s pretend that in 2022 we had a pre tax, pre apportioned $1 million loss for CA. Those three calculations from above would look as follows:

Note the third calculation makes no sense. We expected a 50% provision, and we filed a 47% return. That’s it. We would not adjust the 2022 NOL any further (like we would for say vacation accrual DTA) down to the 2023 apportionment because it is recorded POST apportionment and locked down.

If you are running a blended rate, mixing CA up with a couple other states and applying the rate willy nilly to all DTAs/DTLs including the NOLs, you might get some bad calculations. That’s okay, as long as immaterial.

For 2023, we incur an additional $999,000 pre tax, pre apportionment loss for CA. This is what I commonly see in the deferred provision:

In case you didn’t see, the $1 mil 2022 NOL was adjusted to 40% apportionment, which is technically wrong.

Notice how my tie out return to DTA should be the 869,600*8.84% CA tax rate? Is the difference material, no.

Now, this is a very simple version with one state. Add 35 states with various pre and post apportionment NOLs and will this be material? Probably still no.

Should you chase this difference. Probably no. But you have an explanation to put, because at some point, someone is going to try to tie out your CA NOL balance back to the return and ask you why it doesn’t match. Especially if this is a start up with deep, many year layers of NOLs in the millions for each state. So make a note on your deferred schedule next to the DTA for NOL and get ahead of this concern.

Let’s say that state NOLs DTAs are starting to get large, and none of them tie back to the return schedules because of years of blended rates. What do you do? Figure out how many states to get back to say 60% coverage, and tie out those states and adjust your DTA through the RTP/PY Clean up column.

I tend to dump my apportionment and state rate changes into a return to provision/other item category on the rate rec. Outside of OBBBA and TCJA, I haven’t personally had any changes so extreme that they are material enough to break out. I will only spend the time to get these state apportionment and rate changes categorized correctly for 10K provisions.

Leave a comment